portability estate tax exemption

Tax portability is a helpful tax benefit that should be considered when crafting your estate plan. Please note these laws being permanent means that they are not set.

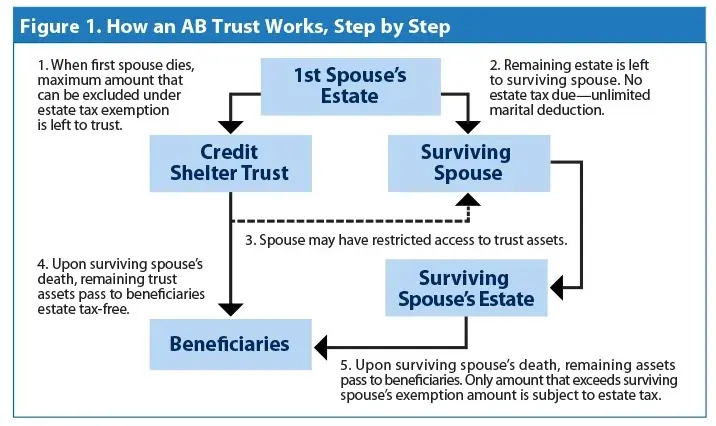

Is Ab Trust Planning Still Effective

The option of portability can make a significant difference when it comes to taxation of an estate.

. Limitations for a properly filed estate tax return is three years. Enter portability of the estate tax exemption. Portability of the Estate Tax Exemption.

That is the IRS has years from the initial three filing deadline to challenge the estate tax return. Thanks to the portability rule the survivor can use whats left. The surviving spouse can use the unused portion of the predeceased spouses estate and gift tax exemption.

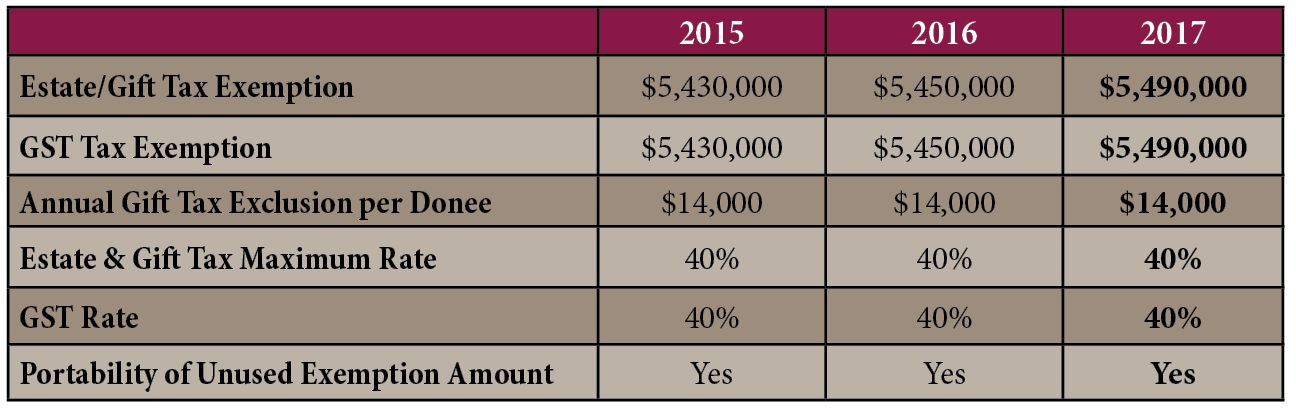

Understanding the portability of the estate tax exemption is crucial to ensuring your spouse has a clear understanding of how portability works. On top of this generous amount the IRS also allows for portability of the exemption between. The estate tax is a tax on an individuals right to transfer property upon your death.

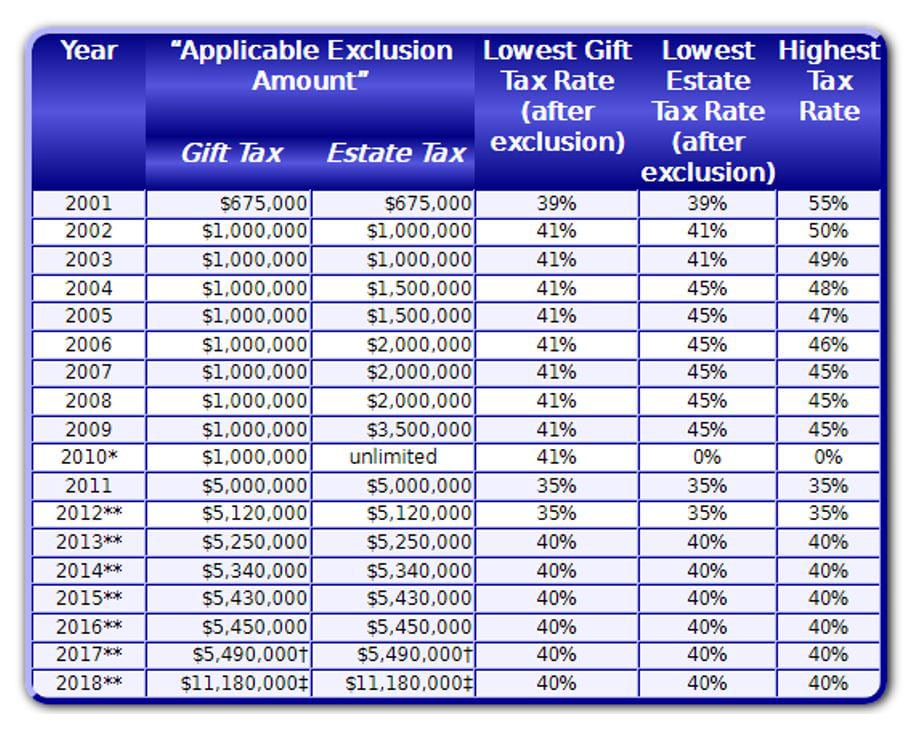

If the decedent made any sizable gifts during his or her lifetime the excess over the applicable threshold for the year of the gift is added back to the estate to determine if the unified federal estate and gift tax exemption is surpassed. In 2010 it increased to 1158 million. If it is there is a 40 federal estate tax on the excess.

This is probably the 1 estate planning concept for married couples. However if the estate tax return includes an election to allow portability of the DSUE amount to the surviving spouse then the time limit on when the IRS can review. So if youre in a state where this type of state estate tax would apply maybe there still needs to be some estate tax planning for both spouses.

Thus with portability Barack Obamas proposal would effectively allow for a 7 million federal estate tax exemption for couples. For 2019 the exemption sat at 114 million. Why You May Want to Transfer Your Unused Estate Tax Exemption to Your Spouse December 17 2019 by Cathy Lorenz.

This means that the exemption moved up to 1118 million per person for the years 2018 through 2025. One is that many states have a state estate tax and in many of those states portability is not available for that state estate tax exemption. John McCains proposal would allow for a 10 million federal estate tax exemption for married couples.

As of 2021 the federal estate tax exemption is 114 million. There are only two states Hawaii and Maryland that have provisions for state estate tax portability as of 2020. In 2022 you will be taxed if the total of the gross assets at hand exceeds 1206 million.

For individuals passing away in 2017 the estate tax is the tax applicable to any amount in the decedents estate over the Federal estate tax exemption of 549 million per person. Also with portability couples would not need to retitle assets to equalize their respective estates. Aside from increasing the estate tax gift tax and generation-skipping transfer tax exemptions to 5000000 for 2011 and 5120000 for 2012 this law introduced the concept of portability of the federal estate tax exemption between married couples.

Portability is a federal exemption. While most states dont have an estate tax some do. How does the Federal Estate Tax Exemption work.

Each year the federal estate tax increases as it is indexed for inflation. For 2019 the exemption has been adjusted for inflation to 114 million per taxpayer and 228 million per married couple. Hawaii and Maryland are two of the few states that allow portability of their state estate tax exemption.

Estate tax planning can be complex. Secondly it only applies to the federal estate tax exemption. Portability of the estate tax exemption The American Tax Relief Act of 2012 ATRA signed into law on January 3 2013 by President Obama extended the opportunities for portability of a decedents unused estate tax exemption.

Since 2010 the portability rule allows any unused lifetime estate and gift tax exemption of a deceased spouse to be transferred to the surviving spouse ensuring it isnt lost. For instance the Tax Cuts and Jobs Act TCJA doubled the estate tax exemption amount. In this post we will discuss probably the most important estate tax election the estate tax portability exclusion.

This is the amount a person can leave their heirs without paying federal estate taxes and which is annually indexed for inflation. Portability allows a surviving spouse the ability to transfer the deceased spouses unused exemption amount DSUEA for estate and gifts taxes to a surviving spouse so long as the Portability election is made on a timely filed federal estate tax return IRS Form 706. Using the concept of portability of the estate tax exemption between spouses under these facts Franks unused 5340000 estate tax exemption will be added to Jennifers 5340000 exemption in turn giving Jennifer a 10500000 exemption.

A surviving spouse can get a big federal estate tax break if the deceased spouse didnt use up his or her individual estate tax exemption. There are many options and exclusion when it comes to minimizing estate tax liabilities. Under portability if the first spouse to die does not use his or her exemption from estate and gift tax the executor of the first spouses estate may elect to give the use of the remaining exemption amount to the surviving spouse the so-called deceased.

Also on January 2 2013 the American Taxpayer Relief Act ATRA for short was signed. The American Taxpayer Relief Act of 2012 ATRA made permanent the portability of estate tax exemption between spouses. That gives the couple a total exemption of more than.

The TCJA doubled the estate and gift tax lifetime exemption from 549 million per taxpayer to 1118 million per taxpayer. The Tax Relief Unemployment Insurance Reauthorization and Job Creations Act of 2010 introduced for the first time the concept of portability of the federal estate tax exclusion between spouses. Portability is the term used to describe a relatively new provision in federal estate tax law that allows a widow or widower to use any unused federal estate tax exemption of his or her deceased spouse to shelter assets from gift tax during the surviving spouses life andor estate tax at the surviving spouses death.

Two important aspects to remember are that the portability exemption is only available to married couples and only applies to Federal estate taxes. In recent years there have been several significant pieces of legislation relating to the federal estate tax exemption.

:max_bytes(150000):strip_icc()/ScreenShot2020-02-03at1.41.37PM-322605a2b23a49598d9cdf9faee0a97a.png)

Form 706 United States Estate And Generation Skipping Transfer Tax Return Definition

This First Installment Of A Two Part Article On Everything Practitioners Should Know About The Estate Tax Includes The Unified Estate T Estate Tax Home Estates

The 2017 Estate Tax Exemption The Ashmore Law Firm P C

Tax Related Estate Planning Lee Kiefer Park

Federal Estate Tax Portability The Pollock Firm Llc

Estate Tax Introduction Video Taxes Khan Academy

Florida Attorney For Federal Estate Taxes Karp Law Firm

Pin By Debbie Wolfe On Trusts Revocable Trust Living Trust Estate Tax

Wsj Tax Guide 2019 Estate And Gift Taxes Wsj

Estate Taxes Under Biden Administration May See Changes

Exploring The Estate Tax Part 2 Journal Of Accountancy

A New Era In Death And Estate Taxes

Historical Estate Tax Exemption Amounts And Tax Rates 2022

Estate Tax Portability Preserving It For The Benefit Of Your Heirs

Estate Tax Exemptions 2020 Fafinski Mark Johnson P A

Grantor Retained Annuity Trusts A Unique Estate Planning Solution Fi3 Advisors

Historical Estate Tax Exemption Amounts And Tax Rates 2022

Federal Estate Tax Facts You Should Know So You Can Pass As Much Tax Free Money As Possible To Loved Ones Karp Law Firm

What Is Portability For Estate And Gift Tax Portability Of The Estate Tax Exemption The American College Of Trust And Estate Counsel